HB 3827, Moving Through the Texas Legislature, Would Leave Texans Vulnerable to Abusive Financial Practices

HB 3827 deals with tech-enabled wage advance products that are marketed as “earned wage access.” Though these new wage-advance products are presented as “earned wage access,” only some are actually based on earned wages. Some models are structured to operate in partnership with employers and collect advances through payroll deduction. But, a large part of the market is based on a “direct-to-consumer” model, offered directly to individuals without involving the employer. These companies give advances through easily downloaded apps based on estimates of future paychecks. Based on average fee charges, these products are very similar to a payday loan.

There could be beneficial versions of these products, including limits on fee charges, but the bill moving through the Texas Legislature enables charges and market practices that would harm Texans who are living paycheck to paycheck. HB 3827 includes vast carve outs from existing consumer protection laws and does not replace those laws with appropriate protections. If enacted, it would open new avenues for abusive financial products, including advances with no maximum fees that are substantially similar to payday loans.

As of the writing of this blog post, the bill has passed through the Texas House and is on its way to the Senate.

About These Products

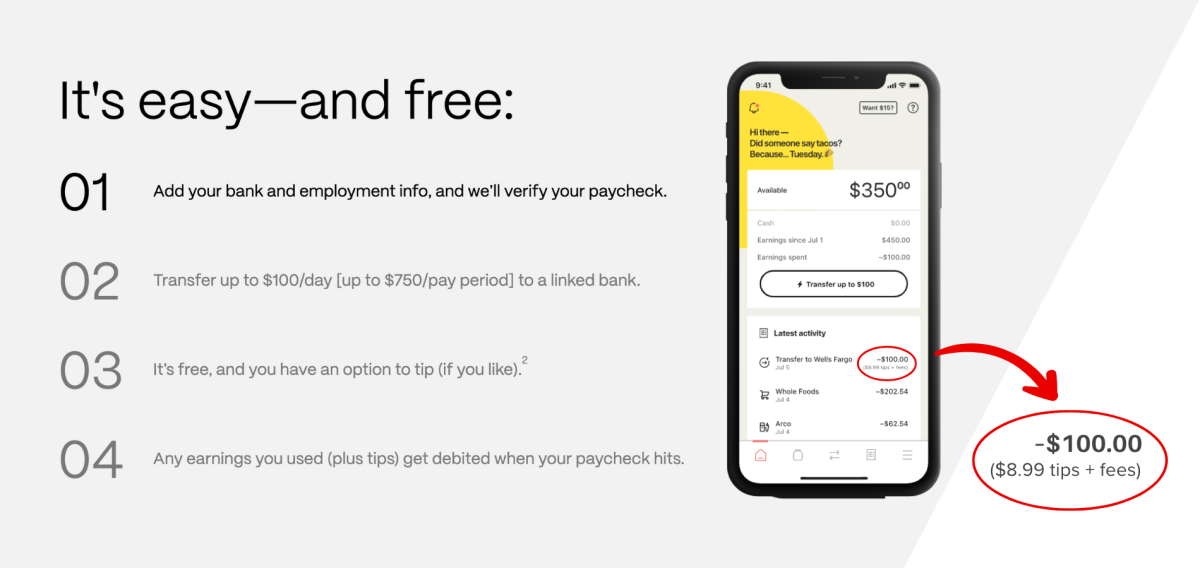

These products are heavily marketed to young, tech-savvy adults who are in need of quick cash. They are advertised as easy and free, but, practically speaking, for most people, the product is not free. For example, one of the biggest companies that offers these types of cash advances has this displayed on their website.

Source: https://earnin.com

There are multiple add-on fees, like the $8.99 in tips plus additional fees shown in the image above. A study looking at total costs associated with millions of these transactions found that they can be astronomical.

Source: 2021 Earned Wage Access Data Findings

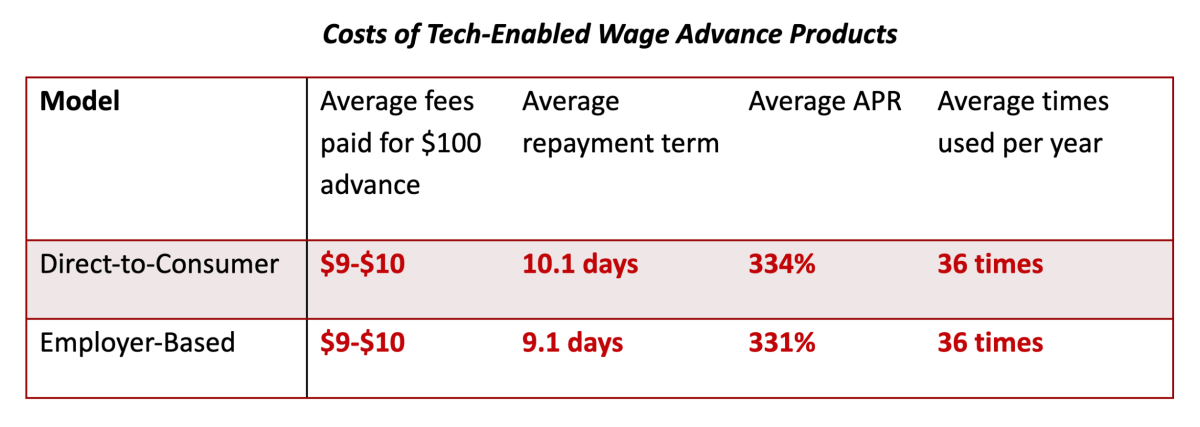

Fees averaging between $9 and $10 for a $100 advance can quickly become a heavy burden for someone already in desperate need of funds, particularly when customers use these products 36 times per year on average! A wage advance has to be repaid from the next paycheck, creating a hole in the person’s budget that requires another advance to fill.

Key Problems

There are a lot of problems with how these products currently work. For starters:

- There are no limits to the number and cost of fees they can charge people to access their services. These companies charge inflated subscription fees, expedited fees, and “tips,” which are disguised interest and charges;

- These companies can debit a payment from the customer’s bank account multiple times until they receive repayment for the cash advance, triggering overdraft and non-sufficient funds fees;

- These companies also pose significant data privacy concerns for those who use the app, and the bill does not include effective accountability to make sure people’s private financial and location information is protected from third-party sales.

There are some positive practices and players in this market, but we can’t shape policy based on the belief that everyone is a good actor. Proceeding too quickly to pass a bill with a lax oversight structure will make it significantly harder to rein in the abuses that will inevitably arise.

HB 3827 Is Bad Policy for Texas

HB 3827 leaves openings for predatory actors to step in and exploit Texans. Under HB 3827, tech-enabled wage advance providers will be allowed to charge unlimited and uncapped fees. Texas has seen this same problem play out with payday and auto title lending, which has drained billions from financially vulnerable Texans and the Texas economy. This proposal to open a new loophole is making its way through the legislature, and critical consumer protections are hanging in the balance. We hope that the Texas Legislature will see these harms and stop the bill from progressing.